If you are thinking about Investments Ireland 2021, you may be wondering how suitable bonds are as an asset class right now. Here’s the rundown on the latest trends in the bond market.

Traditionally, bonds have always accounted for a significant portion of a well-constructed investment portfolio. This fixed-income asset class provides additional diversification for the more turbulent market conditions when stocks falter.

Although bonds still warrant a place in a well balanced portfolio, ultra-low interest rates and general investment market conditions require investors to review their bond allocations, and assess whether they should be reduced.

Read on to find out why.

Latest bond trends – Investments Ireland 2021

Inflation and the Yield curve – Investments Ireland 2021

Effect of bond yields on stock markets – Investments Ireland 2021

Jackson Hole – Late August FED Meeting – Investments Ireland 2021

Where to invest right now? – Investments Ireland 2021

Investment Outlook for bonds? – Investments Ireland 2021

Latest bond trends – Investments Ireland 2021

German 10-year government bonds are currently yielding -0.49%, which means they will lose 4.9% of their value in a 10-year time period, and that is before any inflation considerations. The current ultra-low interest rate environment creates a challenging dynamic for bond investors.

Typically, bonds weaken in response to higher inflation, as inflation eats into the value of the regular fixed interest payments associated with bonds.

On the other side of the Atlantic, 10yr US Treasury notes have rallied since the beginning of April and this has been the source of much confusion for investors, as the pace of US inflation (CPI) continues to worry. These elevated inflation levels have challenged the FED’s view that high inflation during the US recovery will be temporary.

The consumer price index increased 0.5% in July, after climbing 0.9% in June. In the 12 months through July, the CPI advanced 5.4%, the fastest pace since August 2008. Although the CPI data for July decelerated, inflation still remains at significantly elevated levels.

US 10yr Treasury yields have continued to fall during this period, closing out July at 1.22%. Yields move inversely to the price of bonds.

Inflation and the Yield curve – Investments Ireland 2021

The June CPI inflation data initiated a counterintuitive trend within the US government bond market.

The rise of the COVID-19 delta variant and a surprise hawkish tilt from the FED in response to the inflation readings (prospect of “tapering”/reducing the bond buying program), surprisingly led to an increased demand for 10-year Treasury notes, even as the inflation readings were at levels last seen over a decade ago.

The surprise hawkish FED tilt also resulted in a spike in short-dated Treasury yields, resulting in a flatter US Treasury yield curve.

The shape of the yield curve portrays the state of the overall economy. A normal upward sloping yield curve implies stable economic conditions, as yields increase for bonds with higher maturity.

Investors want to get compensated for holding bonds with a longer duration in a normal economic landscape. The recent flattening of a yield curve suggests a more uncertain economic environment and easing inflation concerns, in the anticipation of tighter monetary policy.

Investors have been betting that an adjustment to short-term rates will have the ability to quash inflation concerns in the longer term, leading to the variation in movement between the front and back end of the curve.

Reduced summer trading volume coupled with weaker supply in recent Treasury auctions have also supported the downward trend of 10yr US Treasury yields.

Effect of bond yields on stock markets – Investments Ireland 2021

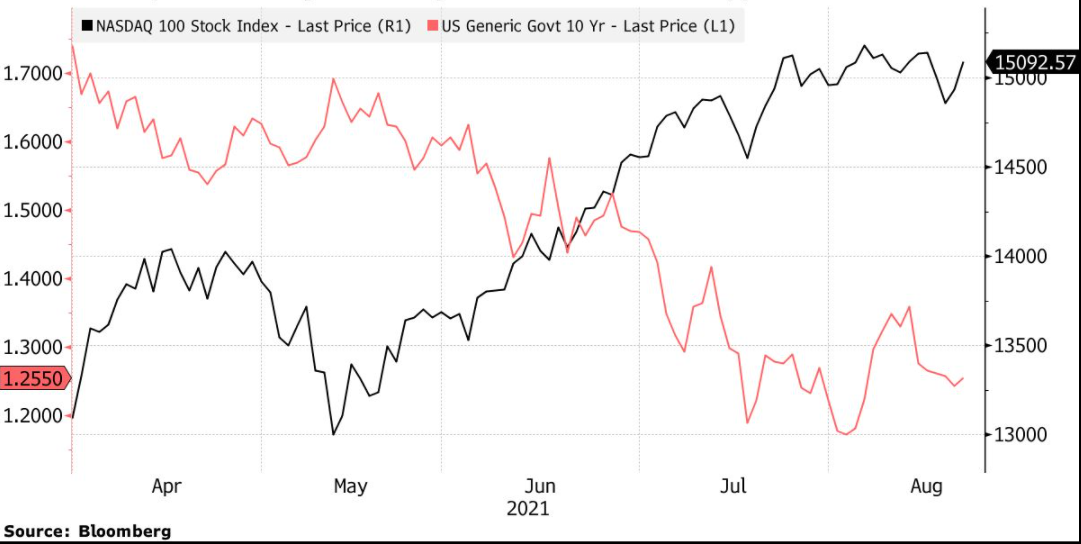

The negative relationship between US 10yr yields and the Nasdaq 100 (Tech) is evident in the chart below [1]:

The recent advance in tech stocks (defensive COVID strategy) came at a time when the price of Treasury bills has risen. The yield on the 10-year Treasury has since fallen nearly a half a percent since the end of March, while the Nasdaq 100 has gained 17% over that period, outperforming the S&P 500 Index by more than 4%.

Jackson Hole – Late August FED Meeting – Investments Ireland 2021

As FED policy makers prepare for another virtual Jackson Hole conference at the end of August, the meeting seems to hold more significance for the global investor community than usual. Any indication that the FED is going to taper the bond buying program is likely to steepen government bond curves, as longer maturity bonds are likely to sell off.

Longer-term interest rates have dominated equity markets over the past year. Investors that expect the 10-year yield to climb in in the latter part of 2021 and into 2022, should be reducing exposure to tech stocks – due to the risk of higher interest rates.

When the 10-year Treasury yield rose to 1.74% during the first quarter of 2021 (rise of 80 basis points), that period also coincided with a significant Growth to Value style rotation within equity markets. The MSCI World Value index rose by nearly 9% during that period, while the MSCI World Growth index barely moved.

This resulted in cheaper (undervalued) equity markets, such as Europe and the UK, outperforming the US. This trend has reversed over the past few months, as the 10-year US Treasury yield plunged to 1.17% by early August, as the fear over the Delta variant gripped global investment markets.

Delta concerns have supported renewed investment in the “stay at home” growth stocks, as they started to outperform again.

Where to invest right now? – Investments Ireland 2021

Investors should be focussing on sectors that are positioned to do well in an increasing yield curve environment, which is one that depicts economic reopening and recovery. The latest viral challenge should be viewed as yet another hurdle along the road to economic recovery, as opposed to a barrier, although the variant may cause a more uneven globally recovery.

Investment Outlook for bonds? – Investments Ireland 2021

According to a recent regulatory filing, Michael Burry, played by Chirstian Bale in the Big Short, has a large short position on long-term (20+ years) US Treasury bills. The options contracts will make money if the value of long-term Treasury bonds depreciate (yields go up). Burry, who was made famous by his very profitable bet against the US housing market, shares the same bearish outlook as many of Wall Street’s elite.

With the Federal Reserve inching ever closer to a “tapering” of its QE bond purchase program, all eyes are once again on the bond market.

Next steps

You can read our more investing in Ireland analysis here.

You can check out our other guides on Investing in Ireland here.

You can find out where to get individual investing in Ireland and financial advice in your area here.