Over the next two months Revolut customers will be offered Irish IBAN numbers for the first time. Although this may sound like a technical change, it’s actually big news.

Why?

Irish IBAN’s were the last thing holding back the two million + Irish Revolut holders from ditching their current accounts with the traditional Irish banks.

Current account switching has been non existent in recent years with the latest figures released by the Central Bank indicating only 0.03% of customers switching their Current Account per year.

Now Revolut customers can simply get their salary paid directly into their Revolut account making dumping the traditional banks much easier.

Technically speaking they should of been able to do this without Irish IBAN numbers under the Single European Payments Directive (SEPA), however many Irish employers never got round to upgrading their IT systems which meant the Lithuanian IBAN used by Revolut before today’s announcement often wouldn’t work.

The Rise of the Digital Banks

Revolut has gained market share more rapidly in Ireland than in any other market in Europe, due to the lack of innovation from incumbent banks, with Ireland now providing almost 10% of Revolut’s world wide customer base.

Other overseas digital banks such as German based N26 and the Dutch based Bunq have also entered the market recently hoping to capitalise on potentially complacency in the traditional Irish banks. Bunq launched Irish IBANs late last year and are also growing rapidly.

These Digital or ‘Neo’ banks, offer lower charges, slicker interfaces and a bevy of features like share trading, crypto trading, junior accounts and saving vaults, that aren’t available from the traditional banks.

With salaries now likely to flow into these accounts, balances are set to rise rapidly opening the door for the digital banks to add the much more profitable lending services such as consumer loans or mortgages.

Competition On The Horizon?

There are still hurdles to this happening, with the famously bureaucratic Irish Central Bank still standing in their way.

With pressure mounting though it now seems that a tipping point may have been reached and real competition across all banking services may finally be on the horizon.

Did you know that money & finance is the most frequent source of worry for Irish adults today, more than family or health? [1]

The source of this worry is financial security. Yet when it comes creating that security, Irish investing and pension participation is less than half UK rates. [2,3]

Why? People need to overcome their financial fears and that’s the problem moneysherpa was born to fix.

My story

Whilst I was responsible for financial services for Ireland’s 3rd largest bank PTSB, I was puzzled by this financial in-action. I couldn’t square the number of people with savings earning no returns or on high mortgage rates and the low levels of switching.

It was only years later, when I started consulting for a financial advice firm, that it dawned on me. The problem was a powerful cocktail of two things, fear of finance and friction in the buying journey.

I got to understand their motivation a lot better by talking to people about their finances over a coffee one on one. In these conversations I’d hear the same themes over and over again.

Savers stuck with earning low returns because they weren’t aware of how to build a portfolio or even better a pension. Mortgage holders sticking with interest rates twice as high as they should be, because they were worried they might lose their house by switching or that the process would be as painful as when they first bought.

Even the people that had overcome this initial fear then found themselves bogged down in tricky choices and paperwork. Giving up before actually making an investment, setting up a pension or switching their mortgage.

In talking to all kinds of people about their finances, I realised that this fear and friction was driven by lack of clear information, impartial advice and supporting services.

Our solution

Existing financial information in Ireland is too wordy and generic. Advice too expensive and compromised, while support to help customers take action easily?

It simply doesn’t exist.

In other countries like the US & UK, customers have already been empowered to take control of their personal finances by startups like moneysherpa. These countries boast 20% higher financial literacy and double the level of financial engagement seen in Ireland [4].

So we assembled a handpicked team of technologists and financial experts and decided to build moneysherpa, to better support the financial journey of Irish customers.

What makes us different

At moneysherpa we empower people to reach their financial goals.

Helping them make smarter decisions and then put them into practice.

We do this by delivering 3 things.

The right information, at the right time. We track what people are actually asking and make sure we give a straightforward answer. Using smart Search Engine Optimisation and our team of qualified expert contributors to produce on point content.

Un-compromised free advice. We provide impartial reviews and recommendations on the best approach and financial providers for our customers. Supported by our strictly impartial editorial code so no financial provider gets unfairly promoted. We are also totally transparent who we get paid by, what for and by how much.

The help they need. We make getting and switching personal finance providers easier. Our on site tools crunch the numbers for you, guiding you to the best rates, the provider most likely to approve your mortgage or working out exactly how much you will really save. Our sherpa customer teams will then guide you through the process of switching mortgage or making an investment over a series of video calls and emails.

Our secret sauce lies in the way we have built our platform from the ground up to solve these challenges for our customers.

Our journey

We have talked to hundreds of customers, jumped over all the required regulatory hurdles, built multiple unique tools and services, then spent hours testing and tweaking all the moving parts. Yet we are only just getting started.

Initially we will be focussed on helping people invest and switch their mortgage. Future developments will see us expand to other financial services, including pensions, savings, loans and insurance.

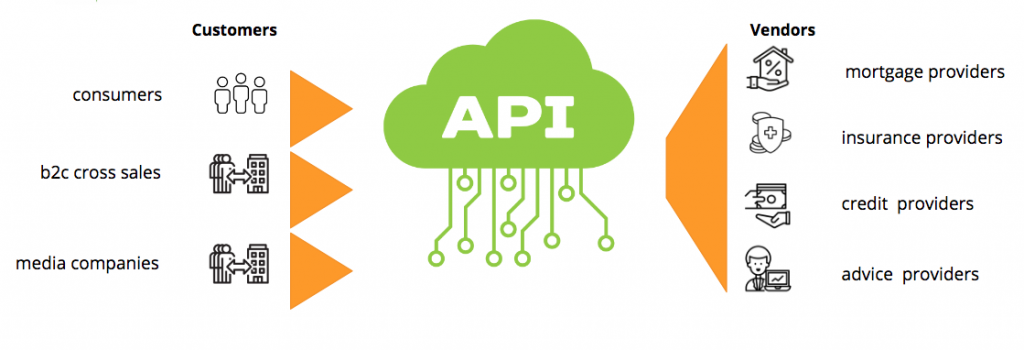

As well as offering our services direct to consumers, we are also able to open up our technology to selected partners using our cloud based architecture.

This will raise the bar for the Irish financial services industry as a whole. We will be announcing our first partners in the coming weeks

What’s next?

If you share our passion to re-shape the personal finance landscape in Ireland, you can follow our progress on our social channels below or by signing up to our newsletter. If you want to suggest a great idea, an article or you are a potential partner you can reach me on mark@moneysherpa.test.inview.ie.

If you want to make smarter investment or mortgage choices, you already know where to go ;-).